The 2014 World Cup came to a dramatic close last night at the Estadio Maracana as a stunning extra-time goal by ‘super sub’ Mario Gotze allowed Germany to claim their fourth World Cup title.

Argentinian fans preyed for their talisman Lionel Messi to provide them with another moment of magic but on this occasion it was not to be and German attacker Mario Gotze stole the limelight. Gotze’s left-footed volley secured the win for the European side – the first time that a European country has won the tournament on South American soil.

****

The triumph of another European ‘Super Mario’ was highlighted last week, as the single currency escaped relatively unscathed from a mini-crisis in the Portuguese banking sector.

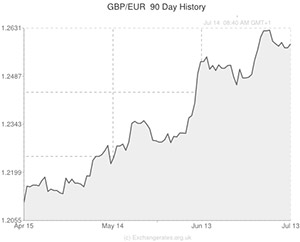

The Pound to Euro exchange rate (GBP/EUR) only grew by around 20 pips last week in reaction to the -17% plunge in Banco Espirito Santo (BES) shares. BES is one of Portugal’s biggest banks and subsequently the flare-up led to a little bit of contagion in the periphery: Italian and Spanish bond yields rose as traders became slightly less confident about the prospect of holding assets denominated in Euros.

The steep decline in BES shares acted as a reminder of the dire situation that the Eurozone found itself in during the darkest days of the Eurozone debt crisis. However, the Euro itself did not suffer any great defeats this time around and Italian 3-year bond yields actually recovered to reach their lowest level since the inception of the single currency on Friday morning.

There are two main reasons why the Euro has remained so resilient in the face of the BES banking crisis. One, Portugal is not considered large enough to have a profound impact on the economic fortunes of the currency bloc at this moment in time. And two, investors have the backing of European Central Bank President Mario Draghi.

Back in the summer of 2012 Draghi massively boosted the appeal of the single currency by vowing to do ‘whatever it takes’ to save the Euro. This one comment alone gave traders the impetus to invest in high-yielding (profitable) Eurozone sovereign bonds without the nasty effort of having to calculate the potential risks involved. If things turn sour, markets know that the ECB’s almost bottomless pockets will be raided to keep any struggling sovereigns afloat.

The fact that GBP/EUR hardly budged in reaction to the news that shares in one of a member states’ largest banks suffered a one-day decline of close to 20% suggests that ‘Super Mario’ Draghi can join his namesake Mario Gotze in celebrating a hard-fought victory.

However, Draghi may have cured the region’s existential crisis but the ECB Chief has not solved the quandary of how to get growth to return to the currency bloc.

Recent easing measures aimed at boosting liquidity to households and businesses have had little time to kick-in yet but it is looking increasingly likely that the ECB will be persuaded to unleash further stimulus over the next few months. Recent comments from Draghi and other ECB policymakers appear to suggest that the bank is on the verge of unveiling a full QE-style Eurozone bond-buying programme.

This will likely drive investors out of the Euro as borrowing costs decline in the 18-nation bloc. The subsequent knock-on effect of a weaker Euro exchange rate should help drive inflation higher in the region and therefore should boost the bloc’s chances of mounting a sustainable return to growth.

If Draghi does opt to initiate a quantitative easing scheme, and if it does succeed in bringing growth back to the Eurozone, then he will surely go down in history, alongside Gotze, as a true ‘Super Mario’.

UPDATED 16:40 GMT 14 July, 2014

Pound to Euro Trading Lower before UK Data

On Monday the GBP/EUR exchange rate softened by 0.32% as investors speculated on the likelihood of this week’s UK reports upping the odds of a Bank of England interest rate hike.

The appeal of the Euro was little affected by a report detailing a -1.1% decline in industrial production in the Eurozone.

If tomorrow’s UK Consumer Price Index shows that inflation is moving closer towards the Bank of England’s around 2% target, the Pound could be supported tomorrow.

Similarly, gains in the GBP/EUR exchange rate could be inspired by disappointing ZEW economic sentiment surveys for Germany and the Eurozone.

Comments are closed.